If you're like most people, paying all the bills each month is very difficult!

If you are barely making ends meet, you might try these tips on how to find extra money each month.

The first step in finding extra money each month is to complete a buget. You need to be very honest with yourself and list everything you are spending money for each month.

Yes, even Starbucks!

Now that you know where you stand, financially, it's time to go to work to see where cuts can be made.

Let's start with you credit card bill or bills.

I know you don't want to hear this, but STOP BUYING THINGS ON CREDIT! I know the rationalization, but if you really want to cut your budget, you cannot justify an extra $10 here and $10 there. It all adds up...way too much!

If you have credit cards with interest rates of 20% or more, you should be able to get them lowered.

Call the credit card company. The number will be on your bill.

When you get the representative on the line, tell them that you must cut your rates and need them to lower yours. If they refuse or say that they can't, tell them (nice way of threatening) them that then you will have to shop around for another creditor to transfer your balance to.

Don't give up! The credit card industry can modify the rates. Obviously, they want to charge as much as possible, so they train their representative to be tough, but YOU HAVE TO BE TOUGHER!

By the way, if you have too much credit card debt and are not able to keep up with the monthly payments, there are several option that may help.

What about that CABLE BILL?

If your not careful, your cable company may slowly raise your bill.

We have a cable company (I won't use their name, but they are BIG!) and have the bundled package (cable, phone, internet, etc.). Our monthly bill is usually about $200. Last month, the bill was $260! That's almost a 30% increase! WHY????

We called the company and was connected to a customer service representative. She said that there was nothing she could do about it, that it was just a "normal" rate increase.

So, we asked to be transferred to the LOYALTY OR CUSTOMER RENTION DEPARTMENT.

Since we had been "loyal customers for so many years...", they said they would not increase our bill! Again, you have to be tough and don't give up!

Utility Bills

It seems that utility companies can get away with raising rates anytime they want to! I know there is some kind of "government application process" each utility company must go through, but when is the last time you saw your rates lowered?

So here's a few tips you can use to cut those utility bills:

Your Heating Bill

We'll talk about how to cut your ELECTRIC or GAS bill later, but first, when is the last time you checked your home for air leaks or drafts?

Yes, you could call a company that does this, but not only will it cost you, most likely they are going to recommend replacing or updating your equipment!

Check all of your windows by feeling for cold drafts of air. If you feel a little cold air, that means that your warm air is most likely going out!

You can get several types of sealers or caulking for windows and doors at your local home improvement store. If your not sure which one you should use, most of the sales reps can help.

What about your old ELECTRIC OR GAS FURNACE?

I'm a do-it-yourself guy, and each time I go into one of our local home improvement stores, there's a sales person trying to get me to "upgrade" my furnance.

Yes, mine is an older model, and yes, the new ones are much more efficient, but I'm having a hard time justifying spend $4,000 - $5,000 to save $30 -$50 on my electric or gas bill!

I know there are government programs that may give me a credit, but I know that by just checking all of my windows, doors, under the sink, etc., I can save a lot of money, and you can too!

WATER BILL

Check for leaks! Just a little faucet drip can end up costing a lot of extra money on your water bill.

Not just the faucets, but check those toilets! If you hear them continuing to run, $$$$ down the drain.

Once again, you should have to call a plumber, but can get great do-it-yourself help online or at your local home improvement store.

INSURANCE RATES

I know you have seen the ads on TV about saving up to 15% on you car insurance, but have you compared your current policies?

Get out your insurance bill (car, home, other) and go on line to compare. I'm not advocating reducing a lot of coverage to save money, but you may not need all of the "extras" you have been paying for.

If you are paying for your own HEALTH INSURANCE, it's time to check it out. Most health insurancd premiums can be dramatically reduced by electing to increase your deductible and/or co-pay.

These are just a few tips on how to find extra money each month, and you may discover more!

What if by just following a few of these suggestions, you could find an extra $50, $100 or more each month? Is it worth it...you bet it is! Good luck!

Debt collectors are paid to get you to pay up.

Debt collectors are paid to get you to pay up.

Confused about Debt Settlement? Here are some easy to understand, basic information about debt settlement that will help.

Confused about Debt Settlement? Here are some easy to understand, basic information about debt settlement that will help. Would you like to know how to improve your credit score?

Would you like to know how to improve your credit score? When you have too much credit card debt, you only have a few options.

When you have too much credit card debt, you only have a few options.  A wage garnishment because of unpaid bills can be devastating!

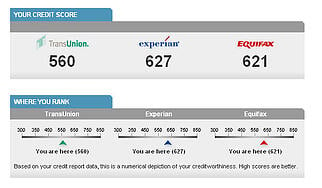

A wage garnishment because of unpaid bills can be devastating! A lady from Portland, Oregon called to ask, "What really determines my credit score?"

A lady from Portland, Oregon called to ask, "What really determines my credit score?" A wage garnishment can be devastating!

A wage garnishment can be devastating!