Losing your job can feel like your whole world is falling apart. A job can be so much more than just a J-O-B, it can define you as a person. When it is pulled out from underneath you with no warning, then your mind set can really be affected. Depression can rear its ugly head during times of high stress and pressure when your personal finances are falling apart.

If you are the main bread winner and you have the responsibility to support your family, loosing a job can soon turn to depression out of feelings of despair and disappointment. Credit card debt, mortgages, and personal loans are all commitments that need to be paid. What happens when you simply don’t have the cash flow?

Keeping a positive mindset is paramount in times of unemployment. You need to look at this as a temporary situation and your new job is to look for a new one. Don’t sit on the couch and dwell on the situation, this doesn’t help anyone. If you just lost your job, and you worked 40 hours per week, then you need to be actively looking for your new opportunity with this time. This is not an opportunity to catch up on reading or cleaning. If you have a family to support or bills that need to be paid, then you must do all you can to get back into work asap!

Ensure your resume is up to date

Rewrite your resume and cover letter and make sure that it contains all your current achievements.

Ensure you have an interview outfit which is clean, ironed and ready to wear. Be ready for an interview at short notice.

Have printed copies of your resume and cover letter with you at all times. Carry a resume folder in your car and bag so that you can drop it off as you find opportune places.

Keeping positive in times of stress and little income

Dealing with debt and stress is not fun for anyone. However, money does not make you the person you are, so don’t let it define you. We all need money to pay bills but don’t focus on the lack. Keep your mind on taking action and applying for jobs.

Be Proactive in looking for new work

Get creative when looking for a new job. Look online and in local newspapers for companies that you would want to work with and make contact with them about future work. Temporary or part time jobs can help you get a foot in the door. Be open to the possibilities of accepting jobs that are outside of your normal industry. You can look for more permanent work in your chosen field while you are working in a less familiar area. By keeping employment gaps on your resume to a minimum, you demonstrate your tenacity and work ethic. By accepting a position that is less than ideal, you may be setting-up your next, better job offer. Remember that employers prefer to hire someone already employed.

Dealing with debt

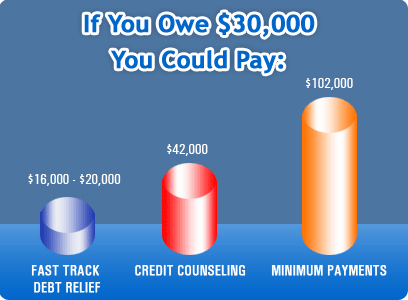

When the debt collectors are calling you for money, and you have little, stress levels can skyrocket. Do not put your head in the sand and ignore this situation. Either answer the phone and discuss your situation with them, or look into your debt relief options. Your debt will not go away on its own. You have options to explore including credit counseling, and bankruptcy as a last resort.

Times of change always present opportunities that may have not have been available before. Be proactive, positive, and keep the lines of communication open. You will get back to work. You will get debt under control. You will regain your life again.

So you’re ready to get out of debt once and for all. The question is, how do you do it and what options do you have. I’m going to share the options available to you as well as the pros and cons of each.

So you’re ready to get out of debt once and for all. The question is, how do you do it and what options do you have. I’m going to share the options available to you as well as the pros and cons of each.

Money is one of the topics couples fight about most often. Debt brought into marriage is an especially troublesome part of many couples’ money problems. Research shows that debt brought into marriage is the number one problem for newlyweds. Unfortunately, debt never rests, sleeps, or goes on vacation and as long as you have debt you will be in financial bondage.

Money is one of the topics couples fight about most often. Debt brought into marriage is an especially troublesome part of many couples’ money problems. Research shows that debt brought into marriage is the number one problem for newlyweds. Unfortunately, debt never rests, sleeps, or goes on vacation and as long as you have debt you will be in financial bondage.

Some great New Credit Card Rules were passed last year. Here's what you need to know:

Some great New Credit Card Rules were passed last year. Here's what you need to know:

What is a 1099-C?

What is a 1099-C?