What legal options can a debt collector exercise in trying to collect an outstanding debt?

What legal options can a debt collector exercise in trying to collect an outstanding debt?

When you do not keep up with the minimum monthly payments due on your credit cards or other unsecured debts, the original creditor may decide to charge the delinquent account off.

It may be transferred to one of hundreds of collection agencies or to a law firm that only specializes in collection of debt.

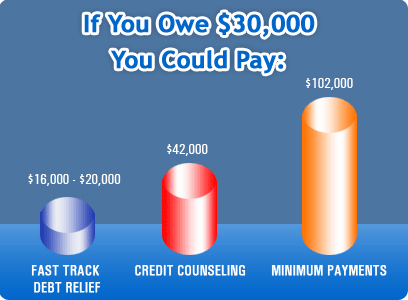

The goal of a settlement program is to negotiate settlements on outstanding debt far below the current balance. This may be anywhere from 35% to 80%, depending on the debt and many other factors.

The first option a debt collector has is to try to get you to pay as much money as possible. They use many illegal methods that violate the Fair Debt Collection Practices Act (FDCPA) such as:

- Frequent and harassing phone calls

- Calling at your place of employment

- Mailing threatening letters

- Making threats of lawsuits or other legal action

- Lying by saying that they never work with 3rd Party Debt Settlement Companies like DRNW, Inc.

We know how annoying these calls can be and have FREE INSTRUCTIONS HOW TO STOP THE CALLS.

The second option a creditor may exercise is to file a claim.

If a reasonable settlement cannot be reached, the creditor or collector may decide to retain a law firm that specializes in debt collection to file a claim.

This is processed with your local county court (usually small-claims court) and you would receive or be served a summons. This is a legal document stating that a claim has been filed against you for the debt you owe.

It will state that you have 20 or 30 days to “answer” the claim. An “answer” is you responding to the claim saying that you do not owe the debt and stating the reason why.

But since 99.9% people who do receive the summons do, in fact owe the money, there is no reason to spend the court fee to file your “answer”.

It is very important that you do not ignore the summons!

If you have received a summons and would like personal, professional help in dealing with it, please let us know!

In most cases, we will work out an agreement in lieu of them going forward with the claim and that will be the end of that.

If a reasonable settlement or agreement cannot be arranged, then the creditor (plaintiff) will be awarded a judgment by default. You do not have to go to court or hire an attorney (unless you decide to dispute the validity of the claim) and they will win the judgment by default.

Once the default judgment has been awarded, not the creditor has a couple of more options:

If you have a job and are paid normal, W-2 income, they may decide to apply for a writ of garnishment in order to have your employer pay a percentage of your paycheck to the creditor until the debt is repaid.

Each state has a little different law, but in most state, that would be 25% of your net, after-tax income. There are also different exemptions that may or may not apply.

If you are self employed it is very difficult for a creditor to get a wage garnishment.

If you are retired, they cannot touch your retirement income (more later).

To prevent the creditor from exercising their legal option ONLY AFTER THE JUDGMENT HAS BEEN AWARDED, you can negotiate an agreement whereby you agree to repay the debt (sometimes at a reduce balance) over time with a payment from your reserve account.

We have many years of experience in helping clients and would be glad to help you also.

Click here for a FREE EVALUATION.

THE IMPORTANT THING FOR YOU TO REMEMBER IS…

A debt collector cannot just decide to garnish you wages without going through the entire legal process and this usually takes several months, giving us enough time to negotiate a settlement or other agreement.

In rare cased, ONLY AFTER THE JUDGMENT HAS BEEN AWARDED, a creditor may apply for a writ or levy to your bank account.

In short, if you are Retired or Disabled, the creditor (again, only after awarded a judgment) CANNOT TOUCH YOUR BANK ACCOUNT!

But, you cannot CO-MINGLE funds in your checking or savings account.

If you work a few hours here or there, win some money at the casino or receive a gift, DO NOT DEPOSIT INTO YOUR BANK ACCOUNT WITH YOUR OTHER RETIREMEN FUNDS!!!!!

Click a link to a great blog of ours about EXEMPT INCOME.

Debt Relief NW, Inc. is not a law firm and does not give legal advice.

Every day we get asked, "What’s the best way to eliminate credit card debt?”

Every day we get asked, "What’s the best way to eliminate credit card debt?”

Sometimes the only way to stop a snowballing problem is to go back to the top of the hill and find out what started it.

Sometimes the only way to stop a snowballing problem is to go back to the top of the hill and find out what started it.

My spouse died. Am I responsible for paying off the debt?

My spouse died. Am I responsible for paying off the debt? In order to pay off credit card debt successfully, it is important to commit yourself to improving your financial situation for the long term. There is no such this as a quick fix. Getting out of debt takes dedication and a realistic plan. With so many options to choose from, it can be overwhelming to figure out where to begin, where to seek advice, and whether you should tackle the debt on your own or enlist the services of a debt relief provider. Let's look at your options.

In order to pay off credit card debt successfully, it is important to commit yourself to improving your financial situation for the long term. There is no such this as a quick fix. Getting out of debt takes dedication and a realistic plan. With so many options to choose from, it can be overwhelming to figure out where to begin, where to seek advice, and whether you should tackle the debt on your own or enlist the services of a debt relief provider. Let's look at your options.

So you’re ready to get out of debt once and for all. The question is, how do you do it and what options do you have. I’m going to share the options available to you as well as the pros and cons of each.

So you’re ready to get out of debt once and for all. The question is, how do you do it and what options do you have. I’m going to share the options available to you as well as the pros and cons of each.

Money is one of the topics couples fight about most often. Debt brought into marriage is an especially troublesome part of many couples’ money problems. Research shows that debt brought into marriage is the number one problem for newlyweds. Unfortunately, debt never rests, sleeps, or goes on vacation and as long as you have debt you will be in financial bondage.

Money is one of the topics couples fight about most often. Debt brought into marriage is an especially troublesome part of many couples’ money problems. Research shows that debt brought into marriage is the number one problem for newlyweds. Unfortunately, debt never rests, sleeps, or goes on vacation and as long as you have debt you will be in financial bondage.