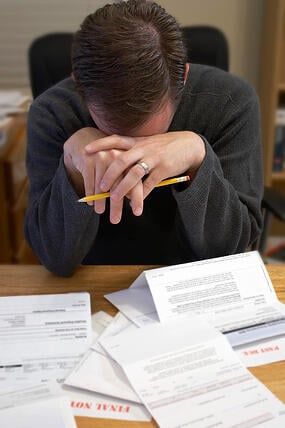

If you have accumulated a substantial amount of unsecured credit card debt, you may be tempted to try Do It Yourself Debt Settlement.

Although it is possible, most people who are inexperienced in dealing with debt collectors end up paying much more than they should.

Why does Do It yourself Debt Settlement end up costing you more?

There are several reasons, but the most important is that debt collectors are for the most part, TRAINED PROFESSIONALS whose only job is to get as much money out of you as possible!

They don't care about your circumstances or why you have fallen behind, and since most of them are paid on commission, they can get mean when trying to get you to pay up.

Collection agencies and Law firms that deal with collections will throw around terms like:

- LEGAL ACTION

- LAWSUIT

- WAGE GARNISHMENT

- LEVY

This scares the average person into agreeing to a monthly payment plan they can't afford or a settlement for 75%-80% of the balance. A reputable Debt Settlement agency knows how to deal with these collectors and how to get you the best deal possible.

Here is a real life example of a settlement that was just completed by our Settlement Specialists:

Our client was a single female and was unemployed for a long period of time. As a last resort, she used her credit cards to buy groceries, gasoline, and sometimes cash advances to pay her rent.

One of her cards was a Visa Card and after charge-off was given to a collection agency. After several unsuccessful attempts to "work something out" with the collection agency, she contacted us to find out what her Debt Relief Options were.

She decided that Debt Settlement was her best option, and our Debt Settlement specialists went to work!

The original balance was approximately $1,400, but after moving around from collector to collector , it was purchased by a "LAW FIRM".

The balance had grown to more than $2,500 as over $1,100 had been added in interest, late fees, and so-called legal fees.

After going back and forth with the collector, our Debt settlement Specialists were able to negotiate the debt down to just $700 which was 50% of the original amount but only 28% of the RIDICULOUSLY INFLATED current balance.

Click Here to See the Actual Settlement LetterYes, it is possible for you to negotiate settlements on your own, but after 10 years of experience in helping hundreds of clients settle debts, avoid garnishment and bankruptcy, I believe in the long run the average person will end up paying much more than necessary.

If you need help settling your debts, our Debt Solutions Specialist are here to help.

1-877-492-4109

Or simply click on the link below for a Free Debt Elimination Analysis!

If you’re struggling with debt, you likely feel like the weight of the world is resting on your shoulders each and every day. Whether it is due to student loans, mortgages, credit cards or other financial struggles, the clutches of debt are enough to make anyone feel trapped and helpless. Luckily, no matter how bad your debt may seem, there are techniques for living debt free.

If you’re struggling with debt, you likely feel like the weight of the world is resting on your shoulders each and every day. Whether it is due to student loans, mortgages, credit cards or other financial struggles, the clutches of debt are enough to make anyone feel trapped and helpless. Luckily, no matter how bad your debt may seem, there are techniques for living debt free.

Debt has the power to overwhelm your life. When the bills start mounting and the collectors start calling, you may feel powerless, disheartened and as though you're in a sinking ship without a life boat. But we at

Debt has the power to overwhelm your life. When the bills start mounting and the collectors start calling, you may feel powerless, disheartened and as though you're in a sinking ship without a life boat. But we at  The doorbell rings and you are handed a summons regarding one of your past due credit accounts.

The doorbell rings and you are handed a summons regarding one of your past due credit accounts. In this economy, Americans are up to their eybrows in debt. In fact, the average American household with at least one credit card has over $10,000 in credit-card debt, and the average interest rate runs in the mid- to high teens at any given time.

In this economy, Americans are up to their eybrows in debt. In fact, the average American household with at least one credit card has over $10,000 in credit-card debt, and the average interest rate runs in the mid- to high teens at any given time. Worrying about your debt won't make it go away, but for millions of Americans the stress from deepening debt is becoming a major pain in the neck - and back and head and stomach! But stressing about your debt won't make it go away.

Worrying about your debt won't make it go away, but for millions of Americans the stress from deepening debt is becoming a major pain in the neck - and back and head and stomach! But stressing about your debt won't make it go away.

We get asked this question nearly every day. So, it's time to answer the question:

We get asked this question nearly every day. So, it's time to answer the question: Whether you ae a shopping addict or use your credit cards to pay your bills, there may come a time when you need help to help organize your bills, repay your debt, and improve your finances. For some, Debt Relief is the answer. But before you jump in head first, it's time for a course in Debt Relief 101.

Whether you ae a shopping addict or use your credit cards to pay your bills, there may come a time when you need help to help organize your bills, repay your debt, and improve your finances. For some, Debt Relief is the answer. But before you jump in head first, it's time for a course in Debt Relief 101.